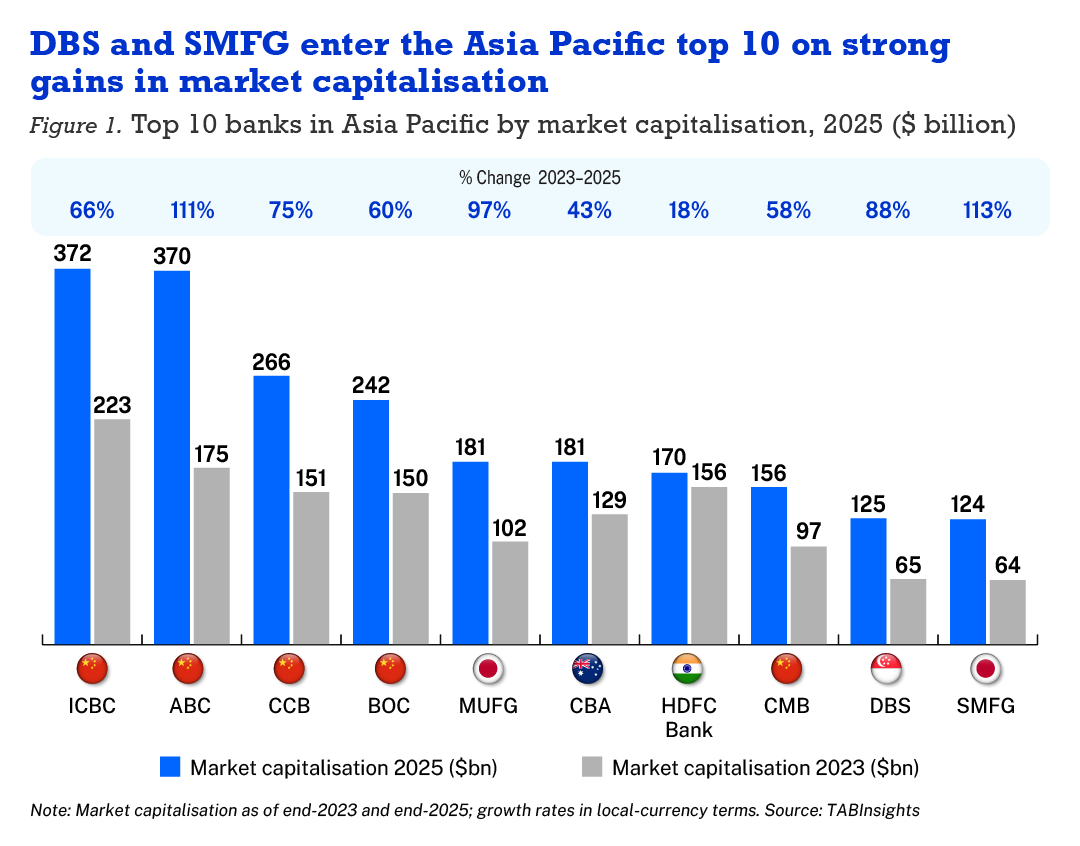

Asia Pacific banks delivered strong gains in market capitalisation between 2023 and 2025, with the combined value of the region’s top 30 banks rising from $2.3 trillion to $3.5 trillion. Improved earnings, resilient economic conditions and capital inflows supported the rally, though performance varied significantly across markets.

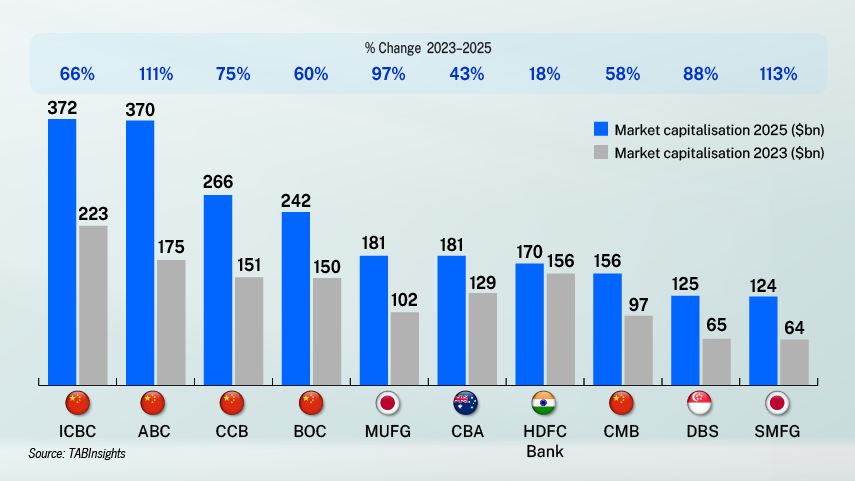

The threshold for entering the top 10 rose from $75 billion to $124 billion, while the top 30 cut-off increased from $26 billion to $32 billion. The top 30 comprises ten banks from mainland China, five from India, four each from Australia and Japan, three from Singapore, and two each from Hong Kong and Indonesia.

Growth was uneven. Japan’s banks in the top 30 recorded a compound annual growth rate (CAGR) of 42% between 2023 and 2025 (all growth rates are in local-currency terms), the fastest in the region. China and Singapore followed at 32% and 27% respectively, while India grew at 13%, and Indonesia contracted by 13%.

Japan’s banking sector outperformance was driven by the Bank of Japan’s monetary policy normalisation, which strengthened earnings and stabilised profitability. A weaker yen boosted overseas earnings and attracted foreign inflows. International diversification reduced reliance on domestic lending. Mitsubishi UFJ Financial Group rose from seventh to fifth, with its market capitalisation up 97% over the period. Sumitomo Mitsui Financial Group entered the top 10 in 2024 and held tenth place in 2025, up 113% over the same period. Mizuho Financial Group recorded the strongest growth among the broader top 30, rising 131% over the same period.

China’s four state-owned giants retain the top four positions. Industrial and Commercial Bank of China (ICBC) remains the region’s largest bank. Agricultural Bank of China (ABC) was the standout performer, rising 111% between 2023 and 2025 to $370 billion, compared with ICBC’s 66% increase to $373 billion. Stable funding, high dividend yields and policy backing from Beijing, which encouraged long-term institutional investment in state enterprises, drove valuation gains across the group.

Indian banks saw rankings decline despite continued growth. HDFC Bank rose to third in 2023 after a re-rating driven by multiple expansion and upgraded earnings expectations post-merger but slipped to seventh by 2025. ICICI Bank grew from $85 billion to $107 billion yet fell out of the top 10. The decline reflected valuation normalisation, softer earnings momentum as margins came under pressure and limited scope for further re-rating after earlier gains. Integration challenges at HDFC Bank and slower valuation gains at ICICI Bank also weighed on performance.

Southeast Asia delivered mixed outcomes. DBS rose 88% between 2023 and 2025 to $125 billion, entering the top 10 in 2025. Strong earnings, cost discipline and higher shareholder returns drove the gain, underpinned by wealth management fees and a regionally diversified earnings base built through acquisitions and investments across Greater China, India and Southeast Asia. In contrast, BCA fell from $75 billion to $59 billion, exiting the top 10. Bank Rakyat Indonesia dropped from $56 billion to $33 billion. These reversals followed elevated US interest rates that triggered capital outflows, weakened the rupiah and tightened funding conditions. Softer commodity prices and moderating demand compounded the pressure, increasing asset quality risks and eroding valuations.

The 2023–2025 ranking shifts were driven more by macro regime than operational merit: monetary normalisation lifted Japan, state capital floored China and rate-driven outflows punished Indonesia regardless of bank-level performance. As policy tailwinds moderate, the extent to which institutions have built durable earnings bases rather than relied on macro uplift may prove the key test of their re-rating resilience.

.png)

.webp)