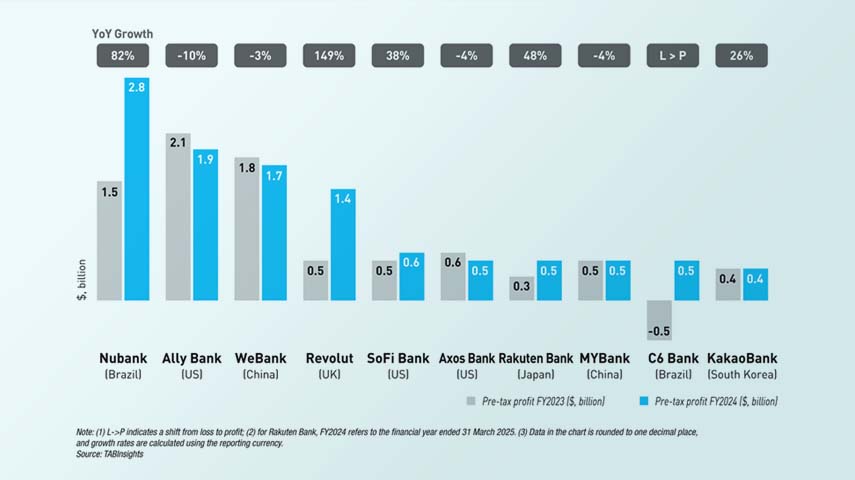

The top 10 digital banks by pre-tax profit in the financial year (FY) 2024 generated a combined $10.8 billion, up from $7.7 billion in FY2023. Nubank, Ally Bank and WeBank led the ranking, with Nubank surpassing both to reach $2.8 billion, supported by diversified revenue streams and operational efficiency. Digital banks have expanded steadily, with more institutions converting scale into sustained profitability.

These top 10 digital banks include three from the United States (US), two from Brazil, two from China and one each from Japan, South Korea and the United Kingdom. While these banks benefit from scale advantages, growth trajectories differ significantly, reflecting variations in strategy, market dynamics and operational priorities. Profit outcomes increasingly depend on disciplined execution, operational efficiency and the ability to diversify revenue streams.

Nubank’s expansion and efficiency drove industry-leading profit

Nubank reached a major milestone by surpassing both Ally Bank and WeBank in pre-tax profit. It became profitable in FY2023, with pre-tax profit rising from $1.5 billion to $2.8 billion in FY2024, up 82% year-on-year, while pre-tax return on equity (ROE) increased from 27% to 40%. This performance was supported by broad market penetration across Latin America, where digital banking adoption remains relatively low. Its customer base grew from 74.6 million in FY2022 to 114.2 million in FY2024.

Nubank’s continued regional expansion and robust digital infrastructure enabled it to scale efficiently while maintaining disciplined cost management. The low monthly average cost-to-serve per active customer of $0.8 demonstrates strong operating leverage, while cross-selling of financial products allowed the bank to monetise its growing customer base more effectively, reinforcing both revenue growth and profitability. In FY2024, it broadened its reach into higher-income segments and launched secured lending, enhancing revenue potential and improving portfolio resilience.

C6 Bank reported its first annual profit of $0.5 billion in FY2024 after several years of losses. The turnaround was driven by stronger product adoption, tighter cost discipline and a strategic shift toward secured lending. Revenue tripled in FY2024, while operating expenses declined slightly. Secured lending accounted for more than three-quarters of total loans, improving asset quality.

Regulatory tightening and margin compression weigh on Chinese digital banks

Two of China’s largest digital banks, WeBank and MYBank, are among the top 10, but both saw slight declines in pre-tax profit in a challenging operating environment. WeBank generated $1.7 billion in FY2024, down 3%, marking its first annual decline since launch. Operating expenses fell 1%, but fee income dropped 18% due to tighter regulatory requirements, while net interest income grew only 0.1% as margins compressed and lending demand weakened. Strategic adjustments toward a more balanced lending structure, including increased micro and small enterprise lending, added pressure to short-term profitability while aiming to optimise the portfolio, manage risk and enhance long-term resilience.

MYBank also experienced a 4% decline in pre-tax profit to $0.5 billion, driven by a 20% increase in loan loss provisions and an 11% rise in operating expenses. Revenue grew 14% in FY2024, largely supported by a 47% increase in fee income as the bank expanded transaction banking services, combining account services, wealth management and payment solutions to create a second growth engine alongside its core credit business.

Ally Bank saw profit dip, while Revolut achieved rapid growth

In the US, Ally Bank, SoFi Bank and Axos Bank rank among the top 10 profit generators, though results reflected structural pressures in a highly competitive market. Ally Bank reported $1.9 billion in pre-tax profit for FY2024, down 10% year-on-year following a 46% drop in FY2023. The decline reflected rising auto loan delinquencies, margin compression, higher funding costs and weaker consumer affordability. Concentrated exposure to auto lending further weighed on performance, contributing to a 9% decline in revenue in FY2023 and a 3% decline in FY2024. Provisions for loan losses also increased by 38% in FY2023 and 9% in FY2024. Ally streamlined operations to sharpen its strategic focus, divesting its credit card business and halting new mortgage originations.

SoFi Bank recorded $0.6 billion in pre-tax profit in FY2024, up 38% year-on-year, delivering strong growth since gaining its national banking licence in FY2022. By contrast, Axos Bank posted $0.5 billion in pre-tax profit, down 4% year-on-year, as higher loan loss provisions limited growth. Revenue and operating expenses rose 15% and 14% respectively.

Revolut delivered one of the fastest profit expansions among global digital banks, supported by rapid international expansion and product diversification. It reached profitability in FY2023 and generated $1.4 billion in pre-tax profit in FY2024, up 149% year-on-year, while pre-tax ROE rose from 32% in FY2023 to 53%. Its services, including investments, cryptocurrency trading and subscription-based offerings, broadened revenue sources and deepened engagement. The customer base increased from 38 million in FY2023 to 52.5 million in FY2024, with monthly active users growing 42% in the retail segment and 56% in business.

By contrast, Starling Bank recorded a 26% decline in profit in FY2024, following 55% growth in the previous year, which prevented it from entering the top 10. The decline was mainly due to a $37 million fine from the Financial Conduct Authority, a $36 million provision for COVID bounce-back loans and rising operational costs from business expansion and regulatory compliance.

Rakuten Bank and KakaoBank leverage platform ecosystems to drive profit growth

Japan’s Rakuten Bank and South Korea’s KakaoBank continued to deliver robust profit growth, supported by strong platform ecosystems and diversified revenue models. Rakuten Bank recorded a 48% increase in pre-tax profit to $0.5 billion in the financial year ended March 2025. Growth in the previous two years was also strong, at 39% and 25% respectively. The bank benefited from close integration with the broader Rakuten ecosystem, including e-commerce and digital payments, which strengthened cross-selling opportunities and customer engagement. Efficient cost management and the Bank of Japan’s interest rate hike also contributed to stronger earnings.

Similarly, KakaoBank delivered robust pre-tax profit growth, rising 37%, 33% and 26% in FY2022, FY2023 and FY2024 respectively. The bank reached 24.9 million customers by the end of FY2024, representing roughly 50% of South Korea’s population, with 18.9 million monthly active users, maintaining high engagement despite slower growth in a market approaching saturation. Non-interest income played a key role in supporting profitability, with fees and platform-related revenue accounting for about one-third of operating income.

The performance of digital banks showcased varied outcomes, with profitability underpinned by scale, diversified revenue streams, operational efficiency and disciplined strategic execution. Some banks, however, experienced profit declines due to factors such as margin compression and regulatory pressures, leading to strategic adjustments. Operational discipline, robust risk management and the ability to monetise customer engagement across multiple services will remain crucial for sustaining profit growth as the sector evolves.

View the full World’s Best Digital Banks Ranking here.

Download the full Databook of the World's Top 100 Digital Banks.

.png)

.webp)