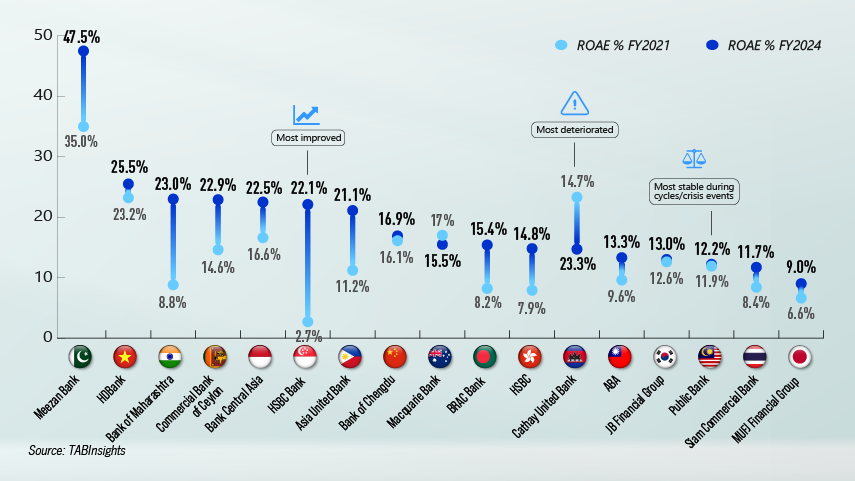

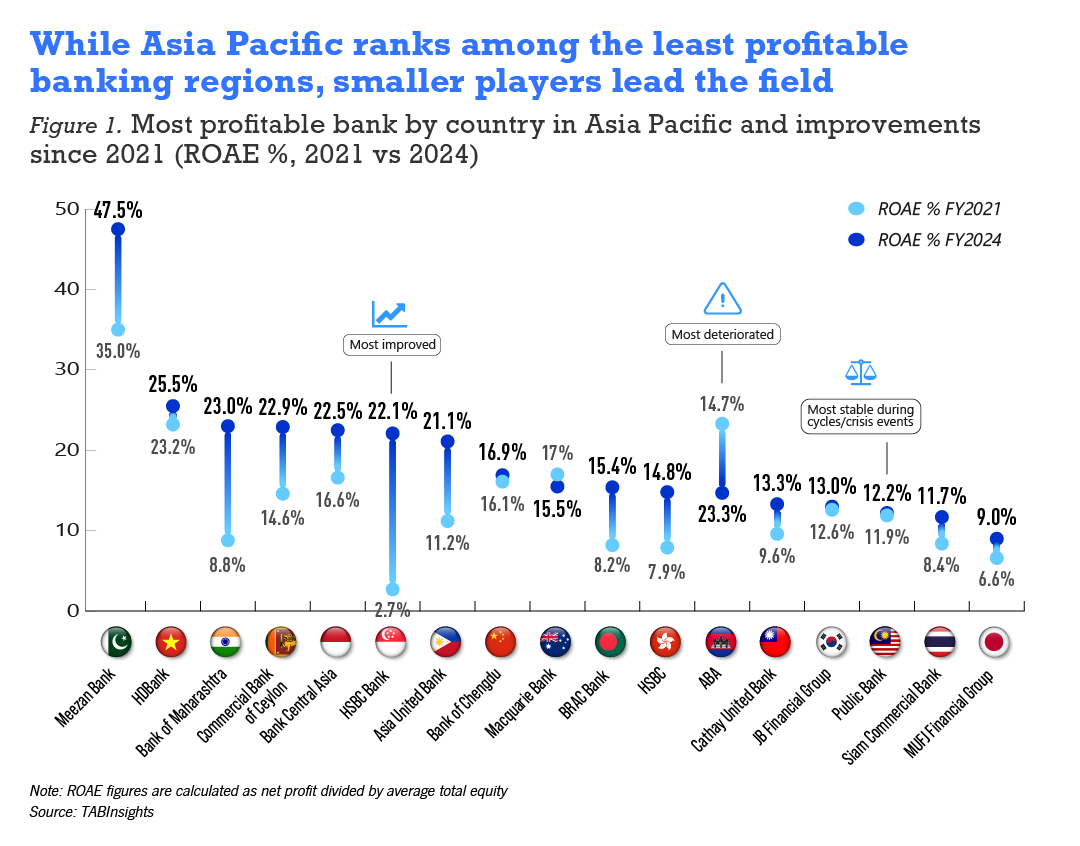

Based on the World's 1000 Largest and Strongest Banks 2025 ranking, Asia Pacific remains the least profitable banking region globally, with an average return on average equity (ROAE) of 8.5%, compared with 12.8% in the Middle East and 15.3% in Latin America. The region's most profitable markets are Pakistan at 23%, followed by Sri Lanka (19.6%) and Vietnam (16.2%). Smaller emerging-market banks — those with assets under $50 billion, spanning 9 of 17 markets — have outperformed larger regional peers over 2021–2024. Only in Hong Kong and Japan do the largest banks rank as the most profitable.

Meezan Bank (Pakistan), with assets of $14 billion, leads with a ROAE of 47.5% in FY2024, up from 35.0% in FY2021. Its Islamic finance focus and operational strength are notable, but these returns must be viewed in the context of Pakistan's macroeconomic conditions. Inflation averaged above 20% from 2021 to 2024, peaking at 38% in 2023, prompting the State Bank to maintain some of Asia's highest policy rates. In such a high-inflation, high-rate environment, banking returns are inflated by wider spreads, loan growth, and higher fee income.

HDBank (Vietnam), Bank of Maharashtra (India), Commercial Bank of Ceylon (Sri Lanka) and Bank Central Asia (Indonesia) all maintained strong ROAE figures above 22%, supported by robust domestic credit demand, high net interest margins, and improving operational efficiency.

HSBC Singapore saw the biggest profitability improvement since 2021

The standout transformation belongs to HSBC Bank Singapore, whose ROAE surged from 2.7% to 22.1% between 2021 and 2024 — the largest absolute gain across the entire cohort.

The global interest rate hiking cycle that began in 2022 and ran through 2023 was particularly beneficial for Singapore-domiciled banking operations. The country's concentration of wholesale banking, wealth management, and international treasury flows left it structurally positioned to capture the rate windfall. HSBC entered from an extremely low FY2021 base, and capitalised on this environment more than any other bank in the country.

HSBC's net interest income (NII) surged from S$461 million ($335 million) in FY2022 to S$736 million ($534 million) in FY2023 — a 60% rise — as the global rate hiking cycle flowed directly through to the bank’s USD- and SGD-linked balance sheet. Overall interest income more than doubled over the same period, from S$561 million ($407 million) to S$1.25 billion ($907 million), while the operating cost base grew only modestly, by around 7%. This produced exceptional operating leverage: total profit after impairments and before tax rose 233% while costs barely moved.

Most stable and resilient performers Public Bank and JB Financial Group

Malaysia's Public Bank and JB Financial Group South Korea are the most stable and resilient performers in this year's analysis.

Public Bank's ROAE moved from 11.9% in 2021 to 12.2% in 2024 — a change so negligible it speaks to full-cycle earnings stability. In a period that encompassed Covid recovery, a global rate hiking cycle, geopolitical disruption, and emerging-market currency volatility, this is a genuine marker of institutional quality.

Public Bank's consistency reflects several entrenched characteristics. The bank has one of the lowest cost-to-income ratios (33.9%) and non-performing loan ratios (0.5%) in Southeast Asia, and maintains a conservatively structured retail- and SME-focused loan book that insulates it from large corporate credit events. Unlike peers who experienced sharp ROAE spikes in the high-rate environment only to face margin compression later, Public Bank's liability structure and depositor base absorbed rate movements without dramatic swings in profitability, making it a benchmark for through-the-cycle resilience in Asia Pacific.

JB Financial Group in South Korea, whose total asset size of $45.2 billion in 2024 was less than 10X the size of Kookmin Bank Financial Group ($513 billion) — is a disciplined regional franchise that outcompetes national giants not through scale, but through specialisation, capital efficiency, and community embeddedness.

It was the only bank among the top nine largest banks in the country that improved its profitability above its 2021 level — from 12.6% to 13% in 2024 — a period that included rate volatility, Korea's property financing crisis, and a sharp tightening of credit conditions nationally. JB's NIM stood at 3.2%, materially above its larger and closest regional peers — BNK Financial at 2.0%.

This spread advantage reflects a deliberate lending mix that focuses on SME and consumer credit within its south-western home regions, segments where relationship-based pricing holds, competition from national banks is less intense, and switching costs for borrowers are higher. What separates JB from peers is not simply that it earns a higher margin — it is that it deploys capital more efficiently and manages costs more tightly. JB Financial's cost-to-income ratio reached a record low of 37.5% in 2024, against a typical CIR of 50–55% among Korea's major banks. The structural basis for this cost advantage is the group's regional concentration. Operating through two anchor subsidiaries — Jeonbuk Bank and Kwangju Bank — within geographically defined home markets means the cost of client acquisition, branch infrastructure, and relationship maintenance is lower than for national banks competing on all fronts simultaneously.

JB Financial's profitability is further underpinned by its non-bank subsidiary, JB Woori Capital, which provides installment finance, leasing, and consumer credit. This migration away from commodity mortgage lending toward higher-margin SME and specialised finance has been the primary structural driver of margin expansion, and distinguishes JB's strategy from regional peers that remain heavily exposed to household real estate lending — the segment most affected by Korea's 2023–2024 property market stress.

ABA Bank Cambodia suffers the steepest decline

ABA Bank — majority-owned by Canada's National Bank and the strongest bank in Cambodia — saw its ROAE fall from 23.3% in 2021 to 14.7% in 2024, the sharpest decline within this top-performing cohort.

The deterioration reflects Cambodia's specific macroeconomic vulnerabilities over this period. The country's highly dollarised economy provided no monetary policy buffer as global rates rose, meaning higher funding costs could not be offset domestically. Cambodia's real estate and construction sectors, historically significant engines of credit growth, experienced stress as foreign direct investment slowed and domestic property demand softened. This raised provisioning requirements and weighed on asset quality metrics.

The Cambodian banking sector also grew more competitive, with a growing number of licensed commercial banks compressing margins. ABA, despite its operational excellence, was not immune to these system-level pressures. Its ROAE, while still robust in absolute terms, reflects a market that has moved from an exceptional high-growth phase toward a more contested operating environment.

Profitability in Asia Pacific is a complex interplay of macro conditions, strategy and balance sheet dynamics

The 2021–2024 period illustrates that profitability trajectories in Asia Pacific banking are highly idiosyncratic. Macro rate cycles, sovereign economic conditions, balance-sheet composition, and strategic execution all interact to produce very different outcomes — even among the region's strongest institutions.

View the complete ranking of the World's 1000 Strongest & Largest Banks.

Download the Databook of the World’s Largest and Strongest Banks here.

.webp)