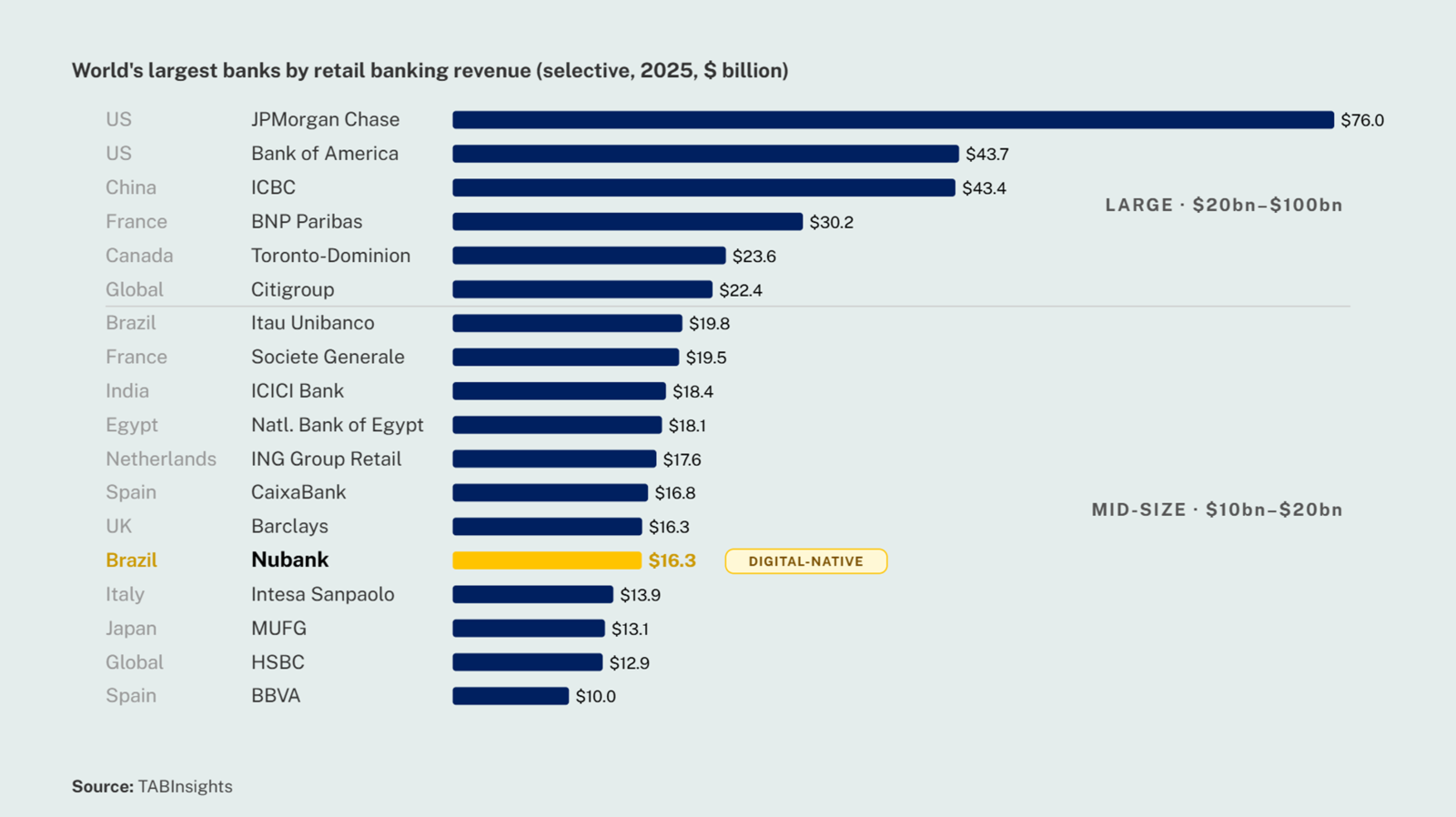

Nubank has already achieved what no digital bank in history has: it has entered the revenue tier occupied by the world's largest retail banking franchises, and it continues to accelerate. For now, management remains focused on strengthening its leadership across Latin America. Brazil is still the core growth engine, where Nubank accounts for about 7% of the country's financial sector gross profit, while its share in Mexico remains below 1%, headroom that CEO David Vélez described as being only "in the first minute of the first half." Mexico and Colombia are the next growth priorities, with monthly average revenue per active customer (ARPAC) reaching about $16 in the first quarter of 2026.

This trajectory reflects more than geographic expansion. Nubank has accomplished what few fintechs have managed to date: sustaining rapid customer growth while delivering consistent profitability and maintaining exceptionally low operating costs.

Its international strategy, however, is unfolding in distinct phases. The US represents a separate and more measured phase of Nubank's expansion. Although the company has received conditional approval from the Office of the Comptroller of the Currency to establish a de novo national bank, Vélez has made it clear that the US business will scale only after achieving clear product-market fit. The strategy is disciplined rather than cautious: validate the model before committing significant resources.

Beyond the US, Nubank's global ambitions begin to take shape. Early discussions in the Middle East and with digital banks in Asia suggest those ambitions are real, even if the timeline remains undefined. What is unfolding is no longer just a Latin American growth story, but the early stages of a structural shift in global retail banking. A sector once dominated by incumbents such as Citibank, HSBC and Standard Chartered is increasingly being challenged by a new generation of digital-first institutions led by Nubank and Revolut.

The financial profile reinforces that strategic narrative. Nubank has achieved what few challenger banks have replicated at scale: expanding loan volumes while increasing customer yield, all while maintaining cost-to-income ratios that remain exceptionally low by the standards of both digital and traditional banks. On the Q1 2026 earnings call, Vélez underscored the significant room for organic growth across its existing Latin American footprint, "Revenue grew nearly 60% year-on-year, we now serve over 135 million customers, and yet we still hold only approximately 7% of the Brazilian financial market's gross profit. We're barely in the first minute of the first half."

That remaining runway is reflected in TABInsights' forecasts. Data from TABInsights show that Nubank is projected to generate $25.6 billion in retail banking revenue by fiscal year 2027, representing a 25% compound increase from 2025. At that level, it would overtake Itaú Unibanco, Brazil's largest bank by assets and one of the world's largest private-sector retail banks, as well as Citigroup's global retail banking business. More importantly, the projection suggests that Nubank is no longer an emerging challenger but a bank operating within the same competitive league as the industry's established leaders. With each quarter of sustained execution, the revenue gap continues to narrow.

Taken together, the question for the next decade is no longer whether Nubank belongs alongside the world's largest retail banks. It already does. The more important question is how far up that ranking it can climb. Nubank is no longer simply a fintech that grew into a bank; it is emerging as a global digital retail banking franchise.

From here, the decisive variable over the next 24 months is no longer Latin America, where the growth thesis is largely de-risked, but the United States. A successful product-market fit there would mark the transition from regional champion to global contender, potentially redefining the competitive hierarchy of retail banking in the decade ahead.

Subscribe for regular insights.

.png)

.png)

.png)

.webp)