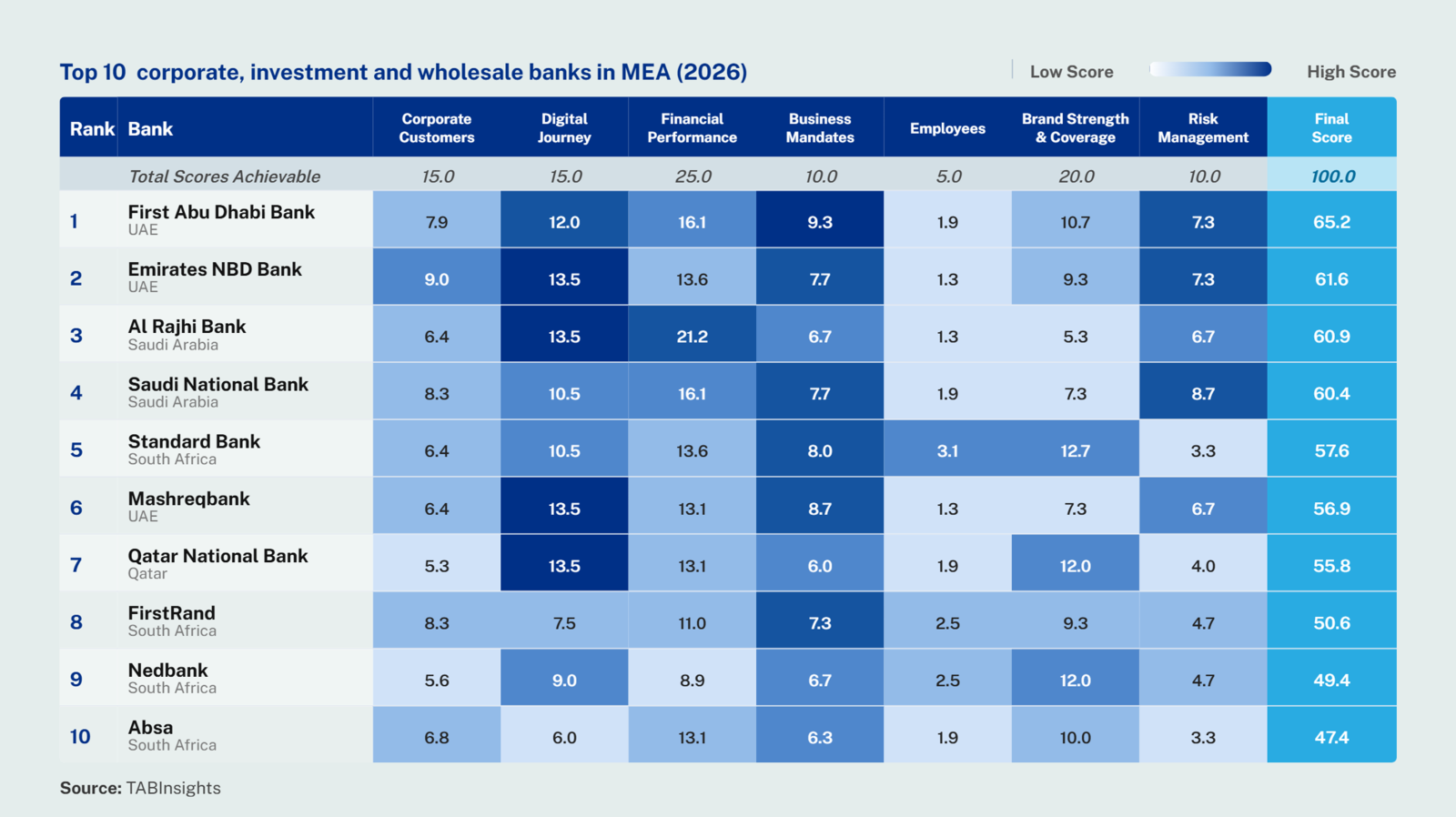

The top 10 corporate, investment and wholesale (CIW) banks in the Middle East and Africa generated approximately $30.7 billion in combined CIW revenues in 2025. The ranking assesses institutions across seven dimensions: corporate customers, digital journey, financial performance, business mandates, employees, brand strength and coverage and risk management.

First Abu Dhabi Bank (FAB) leads the 2026 TAB Global CIW ranking in the region, followed by Emirates NBD Bank and Al Rajhi Bank. While each institution excels in different areas, the top three illustrate the diverse competitive strengths shaping corporate and wholesale banking across the Middle East and Africa.

On CIW revenue, FAB led by a wide margin. Its CIW segment generated approximately $5.0 billion in revenue in 2025, up 14% year on year (YoY), roughly double Emirates NBD's $2.5 billion, which was up 11% over the same period. The bank also strengthened its capital markets franchise by supporting the Middle East and North Africa (MENA)'s first blockchain-based digital bond issuance, a $100 million transaction.

Emirates NBD, meanwhile, distinguished itself through the pace of its wholesale banking expansion. CIW assets grew 34% to $143 billion, compared with FAB's 18% growth to $170.9 billion, although FAB remained the larger franchise in absolute terms. Group-wide, Emirates NBD also grew lending across its Saudi Arabia franchise by 48% during the year, a reflection of its broader geographic expansion rather than growth in the CIW segment itself.

Al Rajhi Bank placed third despite operating a smaller CIW franchise than FAB. The bank generated $2.6 billion in revenue, up 26%, while CIW assets increased 23% to $71.6 billion. It expanded its business-to-business strategic pillar, broadening its corporate banking proposition beyond lending to include trade finance, treasury, investment banking and payments, while its transaction banking cost-to-income ratio (CIR) improved to 19% in 2025, from 31% in 2024.

Saudi National Bank placed fourth, operating one of the region's largest wholesale banking franchises, with $4.7 billion in CIW revenue, an increase of 15%, and $184.9 billion in segment assets, up 12%.

Standard Bank placed fifth, the highest-ranked South African institution. Its CIW segment generated $3 billion in revenue, an increase of 9%, while CIW assets rose 13% to $132 billion and pre-tax return on assets (ROA) improved to 2.5% in 2025, from 2.4% in 2024. Its footprint across 21 sub-Saharan African countries, four global centres and two offshore hubs underpins its ability to support cross-border trade, investment and financing across the continent.

Mashreqbank placed sixth, continuing to strengthen its digital corporate banking proposition with the launch of a corporate API Marketplace for direct client integration. Its CIW segment generated $1.4 billion in revenue, an increase of 1%, while CIW assets increased 30% to $51.6 billion. Despite this strong balance sheet growth, CIW profit before tax declined 10%, while its cost-to-income ratio remained stable at 31%.

Qatar National Bank (QNB) placed seventh, expanding its Digital Bridge Platform to provide businesses with access to more than 20 integrated digital solutions. Its CIW segment generated $4.8 billion in revenue, a decline of 6%, while CIW assets increased 4% to $267.3 billion, making it the only bank among the regional top 10 to report a decline in revenue.

FirstRand, for its financial year ended June 2025, placed eighth. Its CIW segment generated $3.0 billion in revenue, an increase of 0.6%, while segment assets increased 11% to $52.6 billion. Pre-tax ROA remained unchanged at 3.2%, reflecting stable profitability.

Nedbank and Absa rounded out the regional top 10. Nedbank's CIW segment generated $1.7 billion in revenue, up 0.5% with CIW assets totalling $57.9 billion, an increase of 7%, while return on assets fell to 1.4%. Absa's CIW segment generated $2.1 billion in revenue, an increase of 9% with CIW assets reaching $84.5 billion, an increase of 12%, as earnings grew 14% and return on assets held at 1.3%.

Several strategic developments could reshape next year's ranking. Nedbank's proposed acquisition of a majority stake in Kenya's NCBA Group, announced in January 2026, extends its existing Africa Regions cluster into East Africa. FirstRand's planned exit from its UK operations, driven by a motor-finance redress scheme unrelated to its CIW segment, will reduce its exposure outside Africa. Mashreqbank's higher effective tax rate under the UAE's new minimum tax regime has become a standing feature of its cost base rather than a one-off charge.

View the global rankings here.

.png)

.png)

.png)

.png)

.webp)